This is an excerpt from the November/December edition of the Center for Audit Quality’s Audit Committee Insights newsletter series. Read the full edition of this month’s newsletter here. Subscribe to this newsletter series for the latest updates and resources for audit committee members.

We’ve dashed through to the end of the year and we’re even walking in a winter wonderland in Washington, DC this December. This edition of Audit Committee Insights is filled with resources released by stakeholders. Oh, what fun! We’re comin’ to town with the latest collection of regulatory updates, stakeholder resources and hot topics on the horizon to keep audit committees in the know this holiday season. Read on to learn about what’s new.

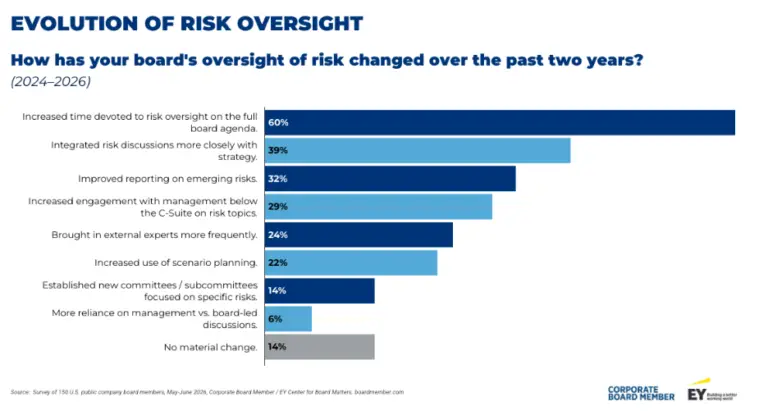

It’s the Most Wonderful Time of the Year: CAQ Releases the 2025 Audit Committee Transparency Barometer

The 12th annual edition of our Audit Committee Transparency Barometer is here and together with Ideagen Audit Analytics, we analyzed public company audit committee disclosures of companies in the S&P 1500. The report includes data from the 2025 analysis, examples of good disclosures, a sample leading practice audit committee matters and report, and questions to consider when preparing audit committee disclosures.

Here are the 2025 key findings:

- 90 percent of S&P 500 companies disclosed the board of directors’ skills matrix, an increase from 85 percent in 2024. S&P MidCap companies (80 percent) and S&P SmallCap companies (70 percent) also showed slight increases.

- 65 percent of S&P 500 boards disclosed they have a cybersecurity expert—representing a 5-percentage point increase from 2024.

- Stagnation and decline of audit committee disclosures (for S&P 500 companies) were observed across several measures, including: disclosure of the annual evaluation of the external auditor (decreased from 39 percent to 38 percent); considerations in appointing or (re)appointing the external auditor (remained flat at 50 percent); and factors contributing to the selection of the audit partner (decreased from 17 percent to 16 percent).

As the role of the audit committee continues to evolve, and disruption in the landscape persists, it is essential to maintain robust disclosures. We encourage audit committees to take advantage of the opportunity proxy statements provide to disclose how the audit committee is fulfilling its oversight responsibilities.

Read the findings and dive into the examples here.

PCAOB Board Member Christina Ho Announces Departure

On December 1, Board Member Christina Ho announced that she would leave the PCAOB by the end of January 2026 after more than four years of service. Board Member Ho currently fills one of the two CPA seats on the board. Read her full statement here.

AI in the Boardroom: Insights for Company Oversight and Committee Operations

The CAQ’s new resource The Role of the Auditor in AI: Present & Future, provides new questions for boards to consider in their AI oversight. If your audit committee is charged with the responsibility of oversight of AI, this is a must read. The resource also suggests questions regarding the current state of AI in the company, strategic objectives related to AI trust and transparency, and how the company plans to achieve those objectives.

Deloitte echoes these focus areas in their newest resource Agile AI governance in the boardroom which summarizes the highlights and actionable guidance from interviews with nine board members across a wide variety of industries, focused on AI governance.

In addition to considering the company’s responsible use of AI, have you considered how to responsibly implement AI within boardroom operations? PwC has many ideas on how to integrate AI into board processes and workflows. Here are a few:

- Put AI use in the boardroom on the agenda: Boards should formally include AI use as an agenda item to facilitate thoughtful discussion about how directors are currently leveraging AI. This discussion could include whether AI will be used for generating queries, performing scenario modeling, drafting minutes or even serving as a virtual observer during meetings.

- Enable secure AI use: Any board-related use of AI should occur within a secure, company-approved environment. Use of personal or public platforms can create significant issues in the tracking and documentation of the board’s activities.

- Maintain human oversight: Outputs from AI carry the risk of “hallucinations” or outputs that sound plausible but lack factual basis. There should always be “humans in the loop” and decision-making should consistently remain with directors.

- Prepare for investor transparency: As AI becomes a more prominent tool in board decision-making, investors may begin to ask how it is being used in governance processes. The board should be prepared to articulate its approach, including how AI informs oversight.

Emerging Technology: What You Need to Know About Quantum Computing

There’s no doubt that advancements in AI are at the forefront of the minds of those charged with governance, but quantum computing is following close behind—or it should be. While classical computers use bits (a code of zeros and ones) to process and store data, IBM notes quantum computing uses qubits which behave like a bit and store either a zero or a one. Qubits can even be a weighted combination of zero and one at the same time.

This unlocks immense potential to revolutionize performance, efficiency, reliability, sustainability and more across industries with quantum computing vendors projecting tangible business benefits by 2030. PwC highlights several specific use cases in their resource Quantum computing: How businesses can prepare for the future and Deloitte explores four potential scenarios companies should consider to help leaders prepare their quantum computing readiness strategy.

This advancement doesn’t come without risks. An article from Grant Thornton suggests quantum computing will be able to break common encryption methods used for cybersecurity and data privacy within the next few years. Although boards don’t need to become quantum experts, Directors & Boards suggests they should be prepared to be knowledgeable and conversant in quantum computing by the end of 2026. Oversight of quantum risk, starting with related cybersecurity risks and data retention, may become a responsibility of the board in the future.

With audit committees becoming increasingly responsible for the oversight of cybersecurity, this is an emerging area to watch.

Three Ways Audit Committees Can Foster a Culture of No Tolerance to Fraud

Participants in the Anti-Fraud Collaboration’s second Fraud Forum emphasized that with quick advancements in and implementation of technology, it’s even more paramount to maintain a strong ethical culture to effectively deter and detect fraud. The forum was hosted in November in collaboration with the CAQ and convened stakeholders from across the financial reporting ecosystem, including boards of directors. Read the summary of the key themes discussed during the event here.

BDO’s recent article A Practical Guide to the Board’s Oversight of Fraud, echoes the importance of a strong ethical culture and emphasizes the crucial function of audit committees in cultivating one of adherence, honesty and accountability to deter fraud within companies. They suggest three ways audit committees can play a role in setting, maintaining, and promoting a culture of zero tolerance to fraud:

- Be visible and accessible to stakeholders and have protocols for the elevation and communication of information to the board.

- Swiftly and fully address conduct and communications that do not align with the company’s code of conduct or culture. Have a protocol for how these instances are identified and responded to.

Consistently speak with one unified voice. Establish clear communication roles and responsibilities for interactions with your stakeholders.