Financial forecasting, always a tricky task, has only become more challenging. Geopolitical events, natural disasters, the economic environment and market volatility are just a few external issues that can derail a company’s best estimates. And since performance objectives are inextricably tied to a company’s business strategy, establishing the right metrics and aligning them to incentive compensation is an increasingly complex task.

Compensation committees set incentive plan performance goals and must not only look ahead at a company’s financial projections and strategic plan but also factor in the potential impact of unpredictable events in the incentive design. For example, just as the pandemic worked out very differently for various industries, ongoing issues like supply chain disruption, rising interest rates and inflation do not impact companies evenly.

“This is playing out in a very industry and company-specific way,” says Jin Fu, a principal at FW Cook. “Even companies that have historically been comfortable forecasting revenue and profit goals for the incentive plan are concerned about the effects of supply chain and labor market issues on the bottom line.”

Addressing Uncertainty

Some boards and compensation committees are reexamining the performance metrics and the mechanics of their incentive plans to recognize the uncertain operating environment.

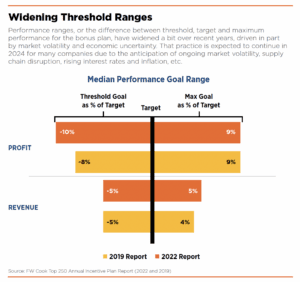

Adjusting the width of the performance range and the slope of the funding line converts the theoretical uncertainty into a more concrete bonus design. “Companies may provide more downside protection for external events by widening the range around the performance goal, for example, from 5 percent to 10 percent below target, to allow for a softer landing,” explains Todd Krauser, a managing director at FW Cook.

This flattening of the slope of the payout curve provides executives with some protection if they fall short of a goal and allows for stretch goal-setting. The additional downside protection is sometimes paired with a de-leveraged upside opportunity, so achievement of the maximum reward is more difficult, though this also depends on the amount of stretch in the performance goal. Balance between downside and upside is beneficial for alignment between performance payouts, which is closely scrutinized by shareholders.

Challenges around goal-setting precision have led some companies to use a “target range” in lieu of a specific goal, which allows for a margin of error. In some cases, this may also be used as a strategy to minimize or soften disclosure language around the occurrence of lower goals than the prior year, which can trigger scrutiny from proxy advisory firms like Glass Lewis and ISS.

There are times when a lower year-over-year performance goal is unavoidable, and disclosing the rationale behind such a change is crucial. Proxy advisors are on the lookout for explicit disclosure about how such lower goals were set and the business rationale for the annual reduction, notes Fu. “Are you able to articulate the reasons that the goal declined in your proxy CD&A to put it in the context of the long-term business plan and provide a supportable defense for shareholders?”

The rationale for a change must be grounded in business strategy, adds Krauser. “Questions that should be considered include: Do your metrics align with drivers of value creation? What is your philosophy for how much stretch is incorporated into the plan? Is it grounded in principles and data? Does it align with metrics used by peers?”

Compensation committees should also regularly review and assess the company’s pay-for-performance alignment. A review of historical performance and payouts is one useful gauge to assess whether prior goal-setting and incentive design was calibrated properly. “Look at how often payments were earned over a 10-year period,” suggests Krauser. “As a rule of thumb, you should expect at least the threshold level to be earned 80 to 90 percent of the time, with the maximum incentive earned one or two times over the last 10 years. If your actual history differs from that, it’s worth understanding why, such as if the company was in turnaround or was a particularly high performer in its industry.”

Reviewing financial performance, incentive metrics and payout slopes against peer companies or similarly-sized industry comparators is another method of vetting the rigor of performance goals. Boards can review the company’s growth rates as well the width of its performance ranges relative to its peers to understand if there is rationale for establishing performance ranges that are wider or narrower than those of its peers. Krauser notes that comparing incentive plan performance results to TSR performance is an effective way to validate pay and performance alignment and to consider if the goals set were actually creating value.

Comparison of performance ranges to market guidance and analysts’ estimates is another consideration. Many companies set incentive plan goals that are consistent with their internal operating budget. In some cases, goals are higher than publicly disclosed guidance, with an incentive earnout threshold near the guidance level so that shareholders are satisfied if any bonus is earned.

Evaluating the rigor of performance goals is critically important to validating the pay for performance relationship.