The five-year plan is under siege in corporate America.

In a stark sign of how dramatically strategic thinking has contracted, only 19 percent of public company board members say their boards conduct scenario planning exercises based on five-year assumptions, according to a recent survey by Chief Executive Group and the Long Term Stock Exchange.

The forces strangling long-term planning are familiar: artificial intelligence’s breakneck evolution, regulatory whiplash and shareholders’ insatiable appetite for quarterly gains. Together, they’ve created what one director described as an environment where leadership teams chase “near-term wins” that often “compromise future positioning.”

Most companies abandoned traditional 10-year planning long ago, retreating to three-to-five-year horizons. Now, even those modest timelines are under siege.

“To go beyond that is very challenging given the rapid change in technology,” says John Ritchie, a veteran technology CFO who has served on several private and public company boards and now chairs the audit committee at Nasdaq-traded MACOM Technology Solutions. He points to AI as the primary culprit, though tax regime changes and regulations like the CHIPS Act have added layers of complexity to capital expenditure planning.

The pressures are crowding out strategic conversations entirely. A director serving on several public and private company boards who asked to remain anonymous, describes a common scenario: “You might have had a strategy discussion with the board and guess what, now you’re talking about tariffs. That’s a reality. Boards are increasingly having to focus on the short term.”

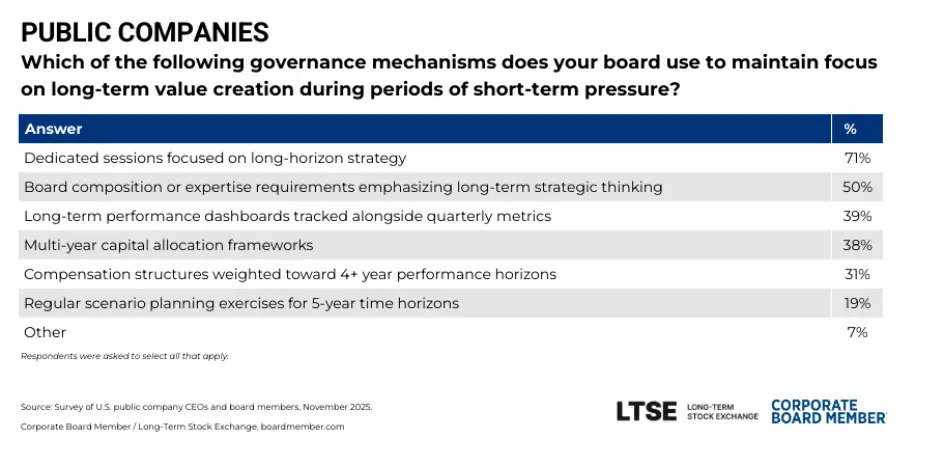

Still, boards bear responsibility for long-term viability, and 71 percent of directors say they support this by holding dedicated sessions on long-horizon strategy. Two-thirds also explicitly tie quarterly financial and operational results to long-term strategic goals—though this practice skews heavily toward larger companies.

Yet certain board decisions demand extended vision. “If you’re talking about tech investment for instance, those sometimes are three-plus-year investments. You have to know, is this the right investment right now from a capital standpoint? As a board, you can’t make that decision unless you know where you’re going,” said one director.

Beyond external shocks—AI disruption, regulatory flux, tariff threats—directors say shareholder pressure on short-term results further “derails and distracts from strategic direction,” as one respondent put it.

Michelle Greene, board member, president emeritus and former Interim CEO of The Long-Term Stock Exchange, a partner in this research, says short-term pressure isn’t a failure of boards but rather the predictable outcome of governance and reporting structures that overweight quarterly signals. “When boards operate within a proven framework that prioritizes long-term strategy, aligned incentives, clear oversight responsibilities and engagement with long-term investors and stakeholders, we consistently see stronger decision-making that supports durable value creation and systemic change.”

Ritchie offers a prescription: “If you create a track record of doing what you say you are going to do in the short term, institutional shareholders may give you flexibility for longer-term objectives. With proven credibility, you could well be afforded the luxury of being able to do more long-term planning.”

The Private Escape Hatch

The first half of 2025 saw 26 take-private deals worth $76.3 billion, according to Dealogic data, with Nordstrom and Walgreens among the marquee names exiting public markets. And while IPOs have since surged, outpacing prior year activity, surveyed private company CEOs cite crucial elements of the public market that continue to drive go-private activity: crushing regulatory compliance costs, relentless shareholder pressure for immediate results and hype-driven valuations that create unrealistic expectations.

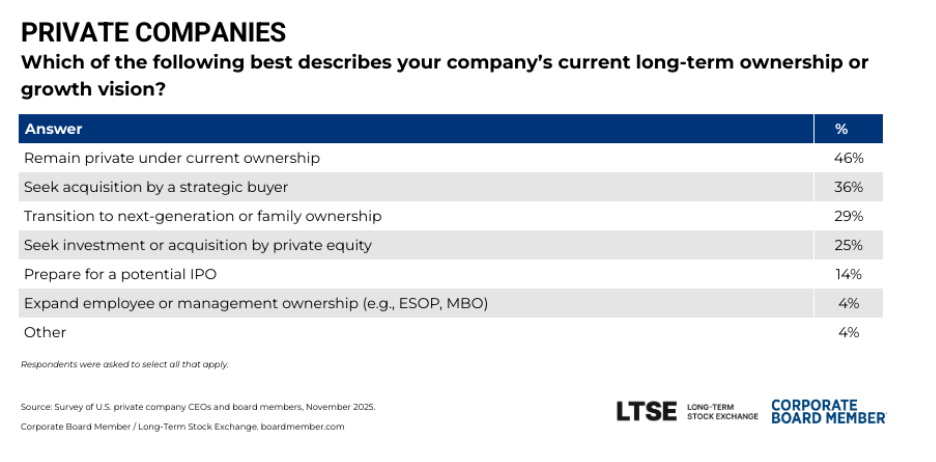

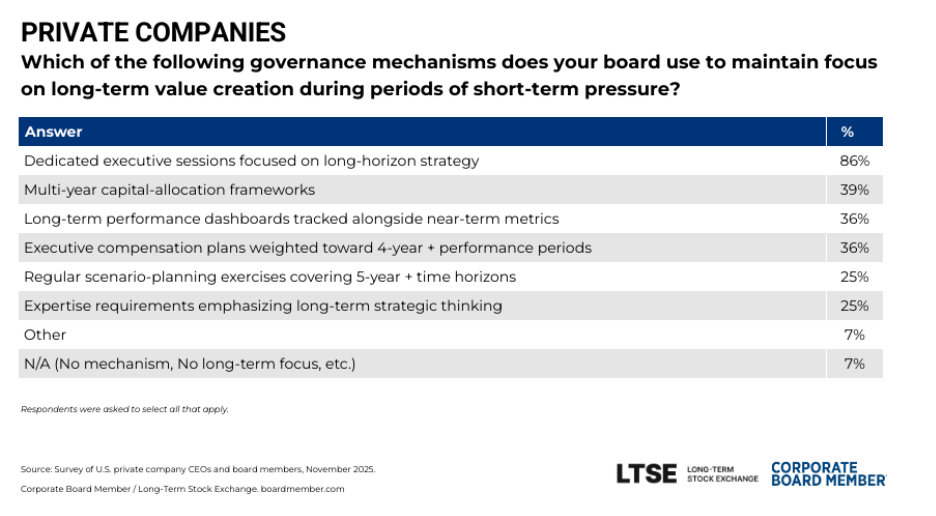

The data suggests that without those external forces, private companies enjoy more breathing room: 86 percent conduct dedicated executive sessions on long-horizon strategy, compared with 71 percent of public companies. Private firms also enjoy what one respondent called “freedom to run a company without the burden of worrying about short-term results.”

But the gulf isn’t as wide as it appears.

Tony Jace spent nearly two decades as CEO of privately held Crisis Prevention Institute before retiring last November. His assessment? “The grass is indeed slightly greener on the private side, but it’s becoming increasingly similar to public markets.”

He describes a demanding accountability structure: “You do have to be accountable on a quarterly basis. Creditors, banks, public analysts, they want to see some type of coherence,” he says. “Sure, you’re not having to be so uber responsive to the questions of the day from analysts, but I still had to present to analysts… I’d talk weekly with our owners. I had an hour call every Friday morning with our owners, and then we had a very deep financial call monthly, and then we had very deep six-hour board meetings with outside directors, the whole thing.”

Three-quarters of private company CEOs surveyed said their long-term vision includes a strategic sale, IPO or private equity transaction. For Jace, this means private companies must embrace public-company discipline. “You have to run a very clean game. You have to realize that it does add some overhead and some inertia that is not fun and does put a bit of a headwind on some of your planning.”

The motivations of owners and largest shareholders largely determine planning horizons. “We’ve always attracted private equity firms that fully understand our mission, our purpose and our culture,” Jace says. “But there are private equity firms that have a thesis, that have done their work and say, ‘These are the nuggets we want to go after. We want to monetize them and in three and a half, four years we’re out.’ It can be quite a shock to the system.”

One director serving on both public and PE-backed boards agrees: “There’s a lot of focus on short-term results in both public and private. As board members, it’s important for us to understand the mindset before you sit on a board so that you’re not unpleasantly surprised by a bias one way or the other. Sometimes the investors clearly have a strategy, and that’s their goal. And if that’s short term, then that’s short term. Your focus is to help deliver for them what they’re looking for.”

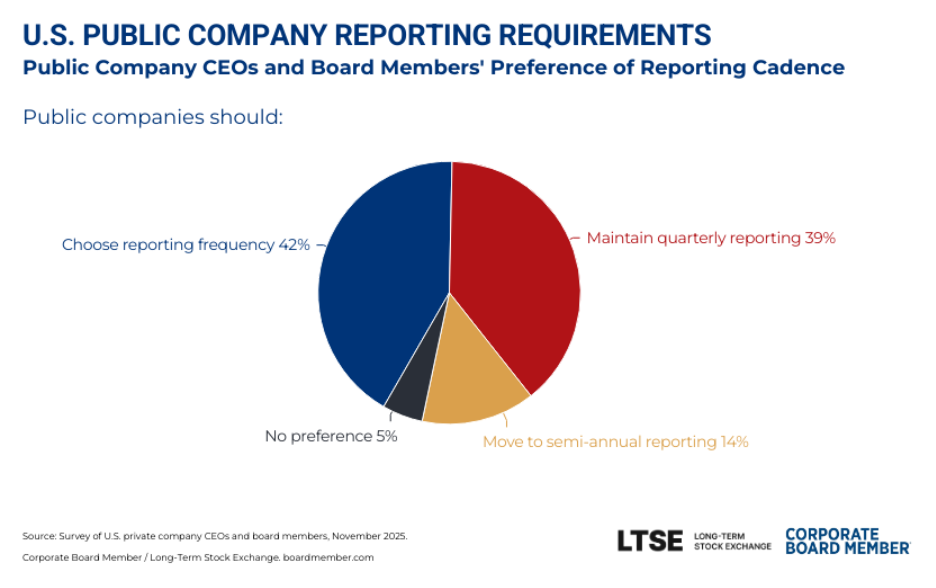

The Reporting Frequency Flashpoint

These tensions have ignited debate over whether public companies should report quarterly or semi-annually. The survey reveals a fractured consensus: 42 percent of CEOs and board members support giving companies the choice, 39 percent favor maintaining quarterly reporting, and 14 percent want a universal shift to semi-annual disclosure.

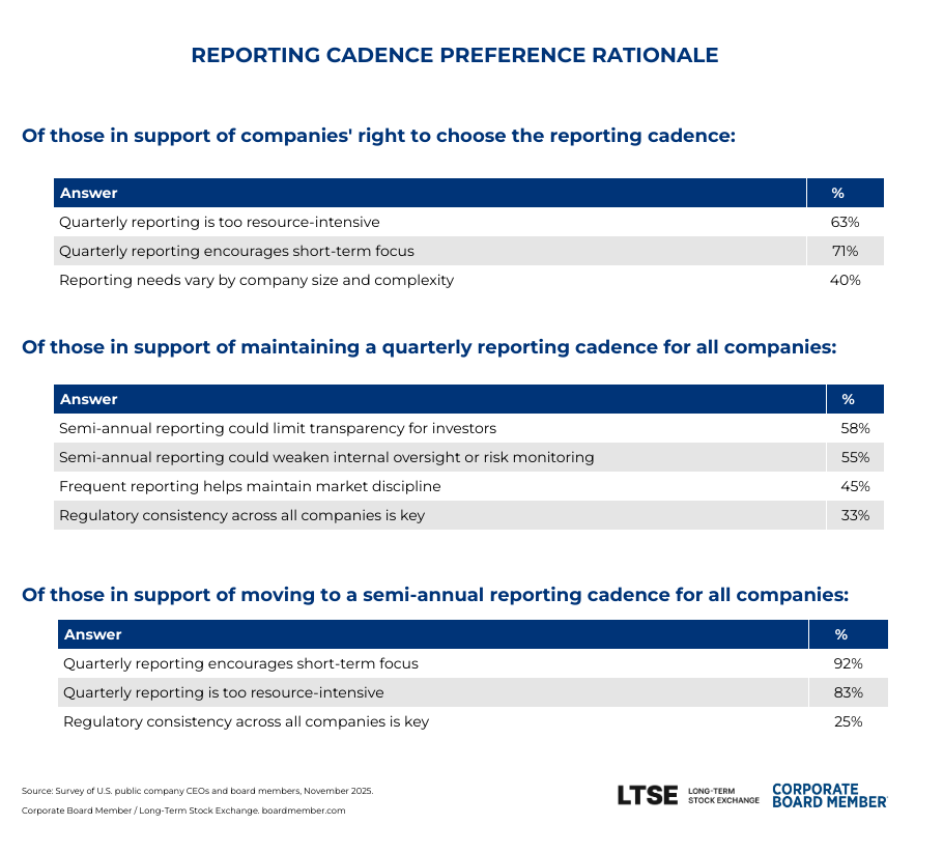

Company size drives the divide. Smaller public companies lean toward semi-annual reporting, with 63 percent calling quarterly reporting “too resource-intensive” and 71 percent arguing it encourages excessive short-term focus—well above the 46 percent overall average.

Larger companies defend the status quo. Among those favoring quarterly reporting, 58 percent worry semi-annual disclosure would limit investor transparency, while 55 percent fear weakened internal oversight. Forty-five percent argue frequent reporting maintains market discipline.

Ritchie acknowledges the burden. “Look at a 10-Q from the ’90s to a 10-Q today. It’s a much more complex document today. And to what end? It’s onerous. If you’re a smaller cap company, those costs can be overwhelming.”

But he opposes letting companies choose. “I would be fundamentally opposed to allowing companies to choose quarterly or semi-annual reporting. If my competitors take six months, they’re going to have a cost advantage. So we’re going to end up becoming a six-month reporting company, too. Whatever market segment that company’s in, that’s going to become the default, and the default’s going to be set by the least disciplined player.”

Maliz Beams, CEO and chair of the LTSE Group Board at The Long-Term Stock Exchange, counters that discipline in public markets doesn’t stem from reporting frequency but from clarity of long-term strategy, transparency around progress and accountability to the right metrics. “Short-term targets matter, but they should function as deliberate mile markers toward long-term value creation, clearly linking this quarter’s performance to a multi-year strategy and sustainable growth.”

But to Ritchie, “the U.S. has the world’s most sought-after and efficient capital markets, period. This is currently based on a rule set of quarterly reporting; it is not perfect, but it’s working.”