The CAQ’s 2025 Institutional Investor Survey obtained insights from 300 investors about how they view the audit, their perspectives on expanded assurance services and their expectations about audit innovation.

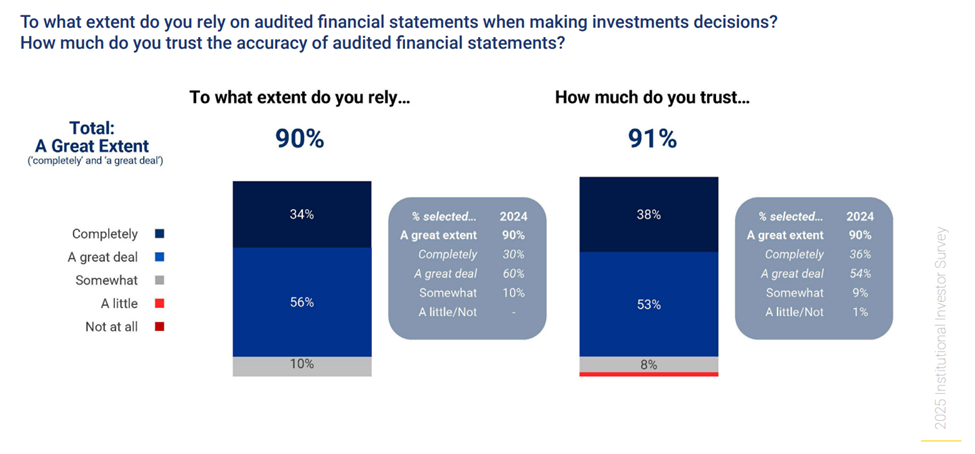

While 91 percent of investors trust the accuracy of audited financial statements, they are actively evaluating whether the same rigor and standards will extend to other areas of corporate disclosure.

For audit committees, three findings stand out.

1. Independence: Audit Committees Are an Essential Safeguard

Thirty-five percent of institutional investors express concern about the audit firm’s independence from management and the company when evaluating the value and reliability of disclosures.

Auditor independence is a fundamental building block of high-quality assurance, ensuring that the information investors rely on is evaluated objectively and free from undue influence and reinforcing confidence in corporate disclosures. In the United States, auditor independence is reinforced by some of the most stringent requirements, established under the Sarbanes-Oxley Act, which set clear standards to protect auditor objectivity and limit conflicts of interest. Still, a sizable minority of investors (35 percent) express concern about maintaining auditor independence.

As the ones responsible for hiring, managing and compensating the external auditor, as well as monitoring compliance with independence requirements, audit committees are the structural answer to this concern. In communications to stakeholders, committees should provide greater transparency into their oversight role to instill confidence among investors.

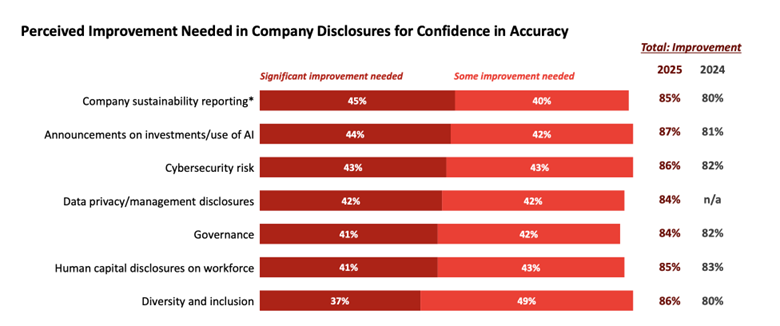

2. Other Corporate Disclosures: How Audit Committees Can Help Deliver Information

Over 85 percent of investors believe improvements are needed in corporate disclosures on AI usage, cybersecurity and other topics. Audit committees are well-positioned to help close this gap as they are increasingly responsible for oversight of disclosures outside of audited financial statements.

Investors already view auditors as a credible source of expanded assurance. Audit committees can accelerate that momentum by ensuring management implements proper quality controls that have been independently reviewed over other corporate disclosure areas.

3. Regulatory Oversight: Quality Over Compliance Volume

Over 95 percent of investors say regulatory oversight increases their confidence in audits, but nearly one-third also believe the current regulatory burden on auditors is too high. Investors want oversight that improves audit quality, not one that adds unnecessary compliance layers.

Audit committees should engage with regulators and standard setters as they explore proposals for expanded assurance to provide critical feedback on how potential rules would impact the profession.

The Bottom Line

The survey is a report on trust: What sustains it and where investors want to see it extended. Audit committees sit at the center of all three dynamics. Proactive engagement and transparency on independence, expanded assurance and regulatory developments isn’t just good governance; it’s how audit committees reinforce the confidence that underpins well-functioning capital markets.

Read the full 2025 Institutional Investor Survey here.