In 2018, Tesla’s board granted Elon Musk a $2.3 billion stock-option package contingent on a 12x increase in market capitalization over 10 years. The award was either the boldest pay-for-performance design in modern corporate history or the most egregious governance failure of its era, depending on your view. Either way, it changed the conversation.

In the years since, more than 50 large public company boards have approved similar though smaller grants. The conventional wisdom on these awards is wrong in an important way.

When compensation committees worry about mega grants, they often worry about whether the performance targets are calibrated correctly. What if the bar is too high? What if the CEO can’t reach it? That worry, it turns out, is misplaced.

After analyzing 58 performance-based CEO mega grants made across the S&P 500, 400 and 600 between 2016 and 2023, we found that almost none of them failed because the design didn’t work. Those that failed did so for entirely different reasons.

The Numbers Boards Should Know

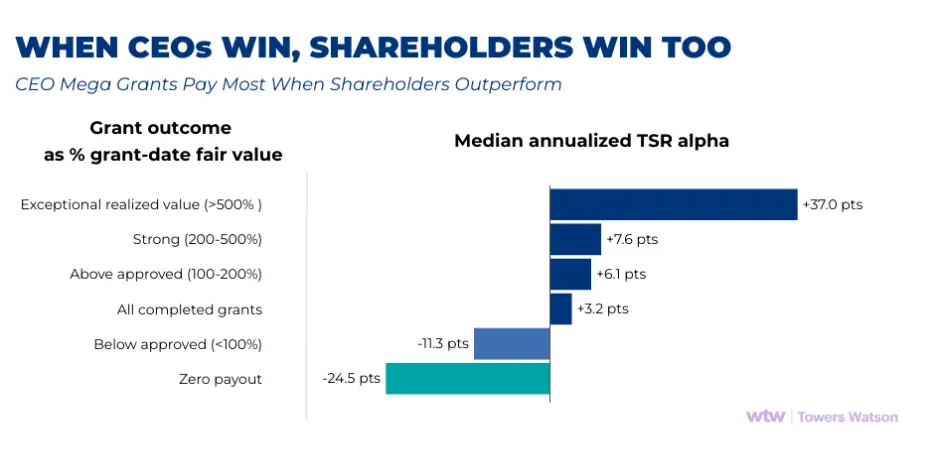

The median completed grant delivered 185 percent of its grant-date Fair Value (i.e., the figure the compensation committee actually approved) while the average delivered 300 percent. More than half of completed grants delivered above the approved value.

Five grants (Tesla, Oracle, RH, Charter Communications and General Electric) delivered five times or more. By the measure that matters most to a board (what we got versus what we signed off on), these grants have on a median basis paid out roughly twice the approved value.

The companies in our sample beat their benchmark indexes in total shareholder return by a median 3.2 percentage points annualized over the performance period. The relationship between CEO payout and shareholder alpha is near-monotonic. Grants delivering exceptional realized value (above 500 percent of grant-date Fair Value) corresponded to companies that beat their index by a median 37 percentage points annualized. Grants delivering zero corresponded to companies that underperformed their index by 24.5 percentage points annualized.

The performance designs did exactly what they were supposed to do: pay generously when shareholders won, pay nothing when shareholders lost. CEOs were not capturing market beta; they were getting paid for genuine outperformance.

Overall, 17 percent of the grants paid out zero, and not one of them failed on performance design. Six of the 36 completed grants delivered nothing. Every zero was driven by something other than the design. Two were forfeited following CEO terminations: Paramount’s grant to Leslie Moonves and PENN Entertainment’s grant to Jay Snowden after the company’s online sports betting strategy reversed. Four were cancelled outright by boards responding to circumstances they hadn’t anticipated: Madison Square Garden Sports following litigation involving James Dolan; PTC when its grant to James Heppelmann “lost retentive value”; IAC during the 2025 transition of Joseph Levin; Paycom when Chad Richison moved to Co-CEO.

None of these CEOs missed a stretch target. They left, were forced out or were repositioned and in every case, the underlying company was also underperforming relative to the market.

Longer-horizon grants performed substantially better. The five grants with performance periods exceeding seven years delivered a median 953 percent of grant-date value, which is consistent with proxy-advisor signals that extended performance and vesting horizons are viewed favorably when paired with meaningful retention conditions.

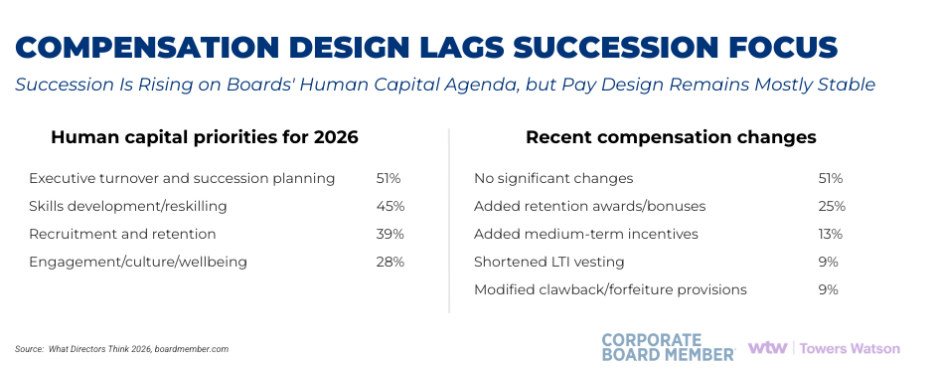

The findings align with what directors themselves are signaling. In What Directors Think 2026, 51 percent of directors said executive turnover and succession planning is likely to demand the greatest board attention among human capital topics this year—and 24 percent identify an unplanned CEO or key executive departure among their organization’s top risks. Yet 51 percent have made no significant changes to their compensation structure in response to shorter executive tenures, and only 18 percent say reviewing the succession plan is a top company priority for 2026. The gap between directors’ stated concerns and their compensation design choices is precisely the territory this data maps.

What Boards Should Actually Worry About

If performance calibration is rarely the failure mode, what is? Three risks deserve more attention than they typically get.

CEO succession risk. Is the executive likely to be in seat through the full period? Are there governance, conflict-of-interest or litigation exposures that could force a separation? Every forfeiture in our sample traces to a question the board may have pressed harder on at grant date.

Board intervention risk. Is there a scenario in which the board itself will need to cancel or restructure the grant because business conditions have shifted, shareholders have revolted or the design has stopped working? Three grants in our sample were materially amended after the fact, each carrying its own optics risk. Investors notice when goal posts move.

Shareholder pushback. Special equity awards have become a primary target of investor concern. Roughly 30 percent of companies that have failed say-on-pay votes in recent years cited a special award as the primary driver. GE’s $57 million grant to Larry Culp contributed to a failed 2021 vote with 42 percent support. Paycom’s $176 million grant did the same. Coty’s $146 million grant to Sue Nabi drew Against recommendations from both major proxy advisors. These are not edge cases.

A Different Recommendation Set

For boards evaluating a CEO mega grant, the data argues for a different set of questions than the ones typically asked.

- Reserve the instrument for genuine transformational situations. Grants framed around clear transformational mandates delivered a median 296 percent of grant-date value with 5.9 points of annualized alpha. Routine retention and recognition uses delivered substantially less.

- Pair market-based metrics with at least one operational anchor. Only 17 percent of grants in our sample do. Pure stock-price designs offer the least protection if appreciation runs ahead of business fundamentals.

- Use performance periods of five years or longer. The data supports this directly, and proxy advisors view extended horizons favorably.

- Pair the grant with an explicit no-additional-grants commitment for its duration. This addresses both dilution and the “floor on pay” optics that drive shareholder pushback when grants underperform—though it will tie the hands of the current and future compensation committee.

- Spend more time on succession and governance risk than on target calibration. The performance design will likely work as intended. The harder question is whether the CEO and the company will be standing where the board expects them to be five to 10 years from now.

One additional finding warrants its own emphasis: for smaller-cap companies, the bar is substantially higher. S&P 600 mega grants in our sample produced a median realized value of zero, with companies underperforming their own index by nearly 18 percentage points annualized. The instrument that works reliably in large-cap transformational contexts has not translated down-market. Smaller-cap boards should either skip the mega grant or invest substantially more in design discipline before proceeding.

The mega grant is a powerful instrument. Used at the right moment, in the right structure, by the right board, it can deliver more economic value to a CEO than the grant-date disclosure suggests—and it tends to deliver precisely because the underlying company is genuinely outperforming the market for shareholders. Used in a routine situation, or in a context where the CEO is unlikely to remain through the period, it concentrates risk in places that performance design cannot reach. The data argues for using the tool carefully and rarely.