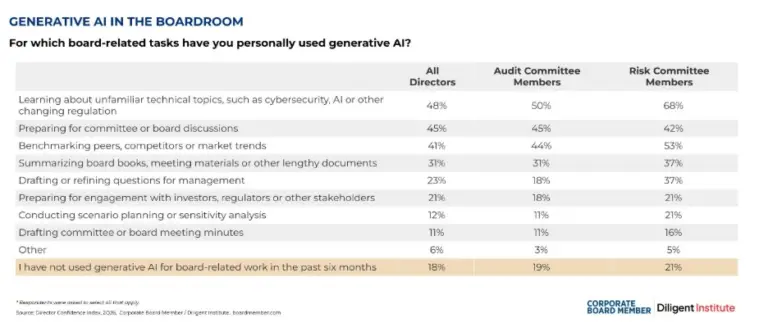

Peer group selection is a critical, and often challenging step in the executive compensation process. The compensation peer group is used to inform the compensation committee and management on the range of practices found in the relevant market that competes for executive talent.

The primary uses of peer group benchmark data include:

- Establishing competitive compensation levels and incentive opportunities;

- Designing compensation and benefits programs and governance policies (e.g., incentive design, severance benefits, stock ownership guidelines, etc.);

- Managing aggregate equity incentive plan share usage and spend.

Ideally, the competitive market for executive compensation levels and design is established based on a group of similarly situated companies with comparable business characteristics (e.g., industry, revenue, market valuation, etc.). However, in practice, the ability to identify a suitable number of peers with sufficient business characteristic overlap is a common challenge. As a result, companies must often look beyond direct industry competitors to identify an acceptable number of compensation peers. Peer group selection methodologies vary in practice, but the following best practice tips will help a company identify an appropriate and defensible group.

Peer Group Development Best Practices

The best practice peer screening process involves filtering a large group of companies down to a relevant group of similarly-sized businesses within related industries and markets on an objective basis as illustrated below.

As a first step, companies should narrow the list to include only companies for which robust executive compensation data is disclosed. For U.S. companies, this would typically mean the selection of companies that are either publicly traded on major U.S. exchanges or private with public debt, as robust compensation disclosure is required for these companies.

Next, an initial universe of potential peers should be identified based on primary and related industries, as these companies will typically have similar executive talent needs and business challenges. Standard & Poor’s Global Industry Classification Standards (or GICS) is the market standard for industry classification. However, it may be appropriate to select peers outside of a company’s industry classification in the event that they exhibit similar business characteristics or have similar business operations.

Once the universe of industry (or related industry) companies has been identified, these companies should be filtered by company size, which is highly correlated with compensation levels (revenues in particular). The most common size determinants for compensation purposes are revenue and market capitalization. These companies will typically be filtered to a range of 1/2x to 2x or 1/3x to 3x of the subject company’s size. However, companies outside of this size range can sometimes be included if they are direct competitors for executive talent or business customers.

Among financial services companies, total assets is a common alternative to revenues for filtering potential peers. The ultimate goal is to narrow down the group to a reasonable number of peers (typically between 15 and 25 companies) with the subject company positioned near the median for the key size measures. A peer group needs to consist of a robust number of companies to ensure it is statistically relevant. The use of too few peers could result in benchmark volatility year-to-year since the influence of a company on benchmark statistics is inversely proportional to the size of the peer group (i.e., compensation changes at a single peer has a more meaningful impact on the market data for a five company peer group compared to a 20 company peer group). However, the use of too many peers could make the benchmark data harder to manage and costlier to compile. (Additional criteria to narrow down the peer group is shown to the left).

Among financial services companies, total assets is a common alternative to revenues for filtering potential peers. The ultimate goal is to narrow down the group to a reasonable number of peers (typically between 15 and 25 companies) with the subject company positioned near the median for the key size measures. A peer group needs to consist of a robust number of companies to ensure it is statistically relevant. The use of too few peers could result in benchmark volatility year-to-year since the influence of a company on benchmark statistics is inversely proportional to the size of the peer group (i.e., compensation changes at a single peer has a more meaningful impact on the market data for a five company peer group compared to a 20 company peer group). However, the use of too many peers could make the benchmark data harder to manage and costlier to compile. (Additional criteria to narrow down the peer group is shown to the left).

Peer Group Selection Pitfalls to Avoid

Public companies are required to identify the executive compensation peer group in their SEC-filed executive compensation disclosure. As a result, companies must have a defensible rationale for why each peer company is appropriate (especially if a unique peer selection methodology has been applied). The following peer selection practices could make this disclosure challenging and should be avoided.

The Use of “Aspirational Peers”

The inclusion of outsized peers (or aspirational peers) may attract negative scrutiny from proxy advisory firms and shareholders as these companies may ratchet the competitive pay benchmarks upward.

“Cherry Picking” Peers

When choosing peers, a company should focus on objective financial criteria and business characteristics of a potential peer as described above. Selecting specific companies (i.e., “cherry picking”) to maximize benchmark pay levels or justify a certain pay practice should be avoided.

The Use of Non-Executive Talent Competitors

Potential peers should be considered if they are labor market competitors for executive talent. Often, there is a more diverse universe of companies that compete for non-executive talent but these companies may not be relevant comparators for executive compensation bench-marking purposes.

Default to Using Valuation Peers

It is common for companies to assume that compensation peers should align with the companies selected by equity analysts or investment bankers for market valuation purposes. Valuation peers often do not comply with the accepted standards used by compensation professionals, proxy advisory firms and major institutional investors when evaluating the appropriateness of peers for compensation purposes.

The development of a compensation peer group can be a challenging undertaking for companies and a point of disagreement between management and its compensation committee. Focusing on the role of the peer group and applying the best practices outlined above can bring clarity to the process. Recognize that it is common for any one peer company to be singled out or criticized as an improper comparator by proxy advisors, individual members of management, or the compensation committee. Therefore, it is important that the peer group be evaluated as a whole to confirm that the inclusion of one or two outliers does not deteriorate the validity of the resulting benchmarks used in the executive compensation decision making process.